We’ll guide you through a brief series of questions online. For example, we’ll ask for details on:

- Your investing timeframe

- How much you plan to invest

- Your feelings about risk

Get matched to an ETF portfolioLegal Disclaimer 1 that’s aligned to your goals and select an account to hold your portfolio. We’ll manage your investments for you.

Open an Account Open an Account

Created with low-cost exchange-traded funds (ETFs), our portfolios (opens modal window) are here to put your money on a mission.

We offer six types of ETF portfolios. Each is available in two versions—Core and Responsible Investing.

What is a Short-Term Bond Portfolio? A professionally managed plan invested in fixed-income ETFs. The portfolio targets low volatility to help smooth out market swings, while providing regular income to gently grow your money.

Is a Short-Term Bond Portfolio right for me? This portfolio is designed for clients investing for near-future goals—like a trip, a wedding, or a down payment. When you open an account and let us know you have a shorter timeline and prefer lower risk, our experts will match you with a portfolio like this one, ensuring your cash stays working and ready when you are.

Why choose InvestEase for your short-term goals? You get the confidence of having licensed portfolio advisors monitor your investments daily, and the ease of tracking your progress right in the app. We handle the strategy behind the scenes, so you can focus on what's next.

| Feature | InvestEase Short-Term Bond Portfolio | Traditional GICs |

|---|---|---|

| Best for... | Flexible timelines. Great if your plans might change (like shopping for a house) and you need your cash ready.Legal Disclaimer† | Fixed timelines. Perfect if you know exactly when you need the money (like a wedding in exactly one year). |

| Access to your money | Not locked in. You can withdraw your money anytime without penalty. | Locked in. Your money stays invested for a set term (usually 1 to 5 years) to earn the guaranteed rate. |

| How it grows | Variable. Aims to provide steady income through lower-risk investments, though your exact return will fluctuate slightly. | Guaranteed. You lock in a specific interest rate, so you know exactly how much you will earn by the end of the term. |

| Risk level | Lower risk. Seeks to limit big market swings, though it is still an investment and not guaranteed. | No market risk. Your original investment (principal) and your interest rate are 100% guaranteed.Legal Disclaimer 6 |

| How it's managed | Actively monitored. Our licensed portfolio advisors monitor and adjust your portfolio daily right in the app. | Set it and forget it. You choose your term, lock it in, and wait for it to mature. |

(All data below as of )

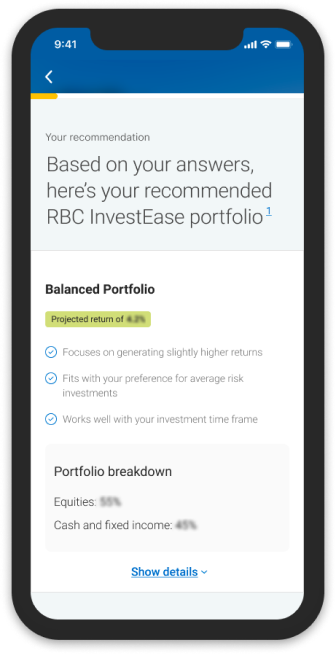

The Balanced portfolio will focus on earning slightly higher returns with a secondary focus on capital protection. The portfolio may include exposure to all asset classes and attempts to balance the allocation between equity and fixed income Exchange Traded Funds (ETF). It carries moderate risk of loss over the investment horizon. Investors who fit this profile generally plan to hold their investments for the medium to long term.

1 mo.

3 mo.

6 mo.

YTD

1 yr

3 yr*

5 yr*

Since Inception**Annualized

*Annualized

[Positions held by the ETFs in the Portfolio]

We’ll guide you through a brief series of questions online. For example, we’ll ask for details on:

Based on how you answer the online questionnaire, we’ll recommend an ETF portfolio for you.

Each portfolio is designed for a specific investor profile and includes a mix of ETFs and cash to meet your goals and risk appetite.

For example, if you’re saving for retirement and want to grow your money as much as possible over 25-30 years, we would likely match you to a different portfolio than if you plan to buy a home in 3-5 years.

While we match you to a portfolio, you get to choose the Core or Responsible Investing version of that portfolio:

Once you have selected your portfolio, you can choose and open your account.

An exchange-traded fund (ETF) is similar to a mutual fund, except an ETF trades like a stock on an exchange. Like a mutual fund, you can buy “units” in an ETF to own a proportional interest in a pool of assets (such as stocks or bonds).

To learn more about how ETFs work please see: https://www.rbcinvestease.com/topics-trends/abcs-of-etfs.html

Indexed ETFs commonly track a specific:

An investment portfolio is a grouping of investments, combined in such a way to meet a specific financial goal and to match a person’s tolerance for investment risk and time horizon.

For example, depending on your reasons for investing and how long you have to invest, your portfolio could be focused on aggressive growth, moderate growth, protecting and preserving your money, or a balance of growth and preservation.

ETFs offer a range of benefits, including:

When you're house hunting, you need your down payment to be safe and easily accessible. The RBC InvestEase Short-Term Bond Portfolio is a great option because it’s invested in lower-risk fixed-income ETFs. It aims to gently grow your money while protecting it from big market swings, and you can withdraw your cash whenever you're ready to buy.Legal Disclaimer†

RBC InvestEase is registered as a restricted portfolio manager in all provinces and territories in Canada, and provides access to model portfolios consisting of RBC iShares ETFs with each model portfolio holding up to 100% of RBC iShares ETFs. RBC iShares ETFs are comprised of RBC ETFs managed by RBC Global Asset Management Inc. (RBC GAM) and iShares ETFs managed by BlackRock Canada Limited (BlackRock Canada). RBC GAM and BlackRock Canada have entered into a strategic alliance to bring together their respective ETF products under the RBC iShares brand, and to offer a unified distribution support and service model for RBC iShares ETFs.

Other products and services may be offered by one or more separate corporate entities that are affiliated to RBC InvestEase Inc., including without limitation: Royal Bank of Canada, RBC Direct Investing Inc., RBC Dominion Securities Inc., RBC Global Asset Management Inc., Royal Trust Corporation of Canada and The Royal Trust Company. RBC InvestEase Inc. is a wholly-owned subsidiary of Royal Bank of Canada and uses the business name RBC InvestEase.

The services provided by RBC InvestEase are only available in Canada.

For FHSA qualified withdrawals, please plan to make the request at least 7-10 business days before you need the funds. This will allow time to complete the required forms, submit the necessary supporting documentation and sell the ETFs and rebalance your portfolio (if required). If you have any questions, please contact us via 1-800-769-2531 or email us at questions@rbcinvestease.com.

All portfolios have been developed by RBC InvestEase Inc. ("RBC InvestEase"). The portfolios include RBC iShares ETFs, with each model portfolio holding up to 100% of RBC iShares ETFs. RBC iShares ETFs are comprised of RBC ETFs managed by RBC Global Asset Management Inc. (RBC GAM) and iShares ETFs managed by BlackRock Canada Limited (BlackRock Canada). RBC GAM and BlackRock Canada have entered into a strategic alliance to bring together their respective ETF products under the RBC iShares ETF brand, and to offer a unified distribution support and service model for RBC iShares ETFs. As such, the RBC iShares ETFs are related or connected issuers of RBC InvestEase.

Your money will not be invested until your account balance reaches $100 or more. Small balances (less than $1,500) may be allocated to a Starter Portfolio that invests in a limited selection of RBC iShares ETFs and/or cash. Our Starter Portfolios follow similar risk profiles to our Core Portfolios while investing in fewer RBC iShares ETFs.

Performance Disclosure

The returns and performance information presented represents the composite performance return of each of the Core Portfolios and Responsible Investing Portfolios that are available at RBC InvestEase as of the date noted. The composite performance return includes all portfolios having a common investment objective and strategy, but excludes all Starter Portfolios.

Performance returns for the Core Portfolios are calculated from June 2, 2019. Performance returns for the Responsible Investing Portfolios are calculated from June 2, 2019. A percentage of each of the representative portfolios may be invested in cash from time to time, with the remainder invested in ETFs. Holdings and asset class weightings will vary per the objective and strategy of each representative portfolio, and may change at any time without notice. The calculated rates of return represent historical total returns, which include changes in the value of the investment units and any distributions received. These returns are gross of fees and taxes, meaning they do not account for sales charges, redemption fees, optional charges, management fees, or income taxes. The rates of return are computed using a time-weighted methodology, excluding the impact of cash flows (such as deposits or withdrawals). Returns are expressed on a total return basis, reflecting both capital appreciation and reinvested distributions. Calendar returns represent the average change in the investment over a calendar year and across a multi-year period. Commissions, trailing commissions, management fees and expenses may be associated with investing in exchange-traded funds (ETFs), please refer to the prospectus before investing.

The information presented is provided for informational purposes only. All return values, charts and other demonstrative content are provided for illustrative purposes only. The information provided does not constitute and should not be construed as advice of any kind. Every effort has been made to ensure the information presented is correct at the time of publication, however RBC InvestEase cannot guarantee the accuracy or completeness of the information, as errors and omissions may occur. Any upward or downward trend presented is not an indication that the representative portfolio is likely to increase or decrease in value at any time. Past performance is not indicative of future results. Future returns are not guaranteed, and a loss of original capital may occur. To the full extent permitted by law, neither RBC IE nor any of its representatives or affiliates, accepts any liability whatsoever for any direct, indirect or consequential loss arising from, or in connection with, any use of the information provided.

Dividend Yield: The dividend yield is a measure of the latest ETF distribution amount per share divided by the ETF price per share as of the date of this document while taking into account the relevant asset mix data in the RBC IE Core Portfolios or RBC IE Responsible Investing Portfolios, and is expressed as an annualized percentage.

MER is based on the collective fees, expenses (excluding commissions and other portfolio transaction costs), and GST/HST paid by the underlying ETFs in the portfolio for the preceding period, including any ETF’s proportionate share of the MER, if any, of any underlying fund the ETF has invested in, and is expressed as an annualized percentage of average daily net asset value during the period. For more information on the range of weighted-average management expense ratios applicable to the ETFs held in RBC IE portfolios, please refer to Pricing at https://www.rbcinvestease.com/.

Many GICs are guaranteed by the Canada Deposit Insurance Corporation (CDIC) for up to $100,000 (this includes both principal and interest), provided that certain criteria are met. Visit the CDIC website to learn more about coverage.

Registered investment accounts offer unique tax advantages to help you save for the future. The features, benefits and rules for registered accounts are determined by the Government of Canada.

Registered investment plans offer unique tax advantages to help you save for the future. The features, benefits and rules for registered plans are determined by the Government of Canada.

With the federal government's Home Buyers' Plan, you can use up to $60,000 of your Registered Retirement Savings Plan (RRSP) savings ($120,000 for a couple) to help finance your down payment on a home.

To qualify, the RRSP funds you're using must be on deposit for at least 90 days. You must also provide a signed agreement to buy or build a qualifying home.

The best part is the withdrawal is not taxable as long as you repay it within a 15-year period. The payback amount is at least one-fifteenth a year of the amount you withdrew from your RRSP.

ETFs are designed to hold stocks and bonds in a single container. That container is a fund you can buy.

While they're similar to mutual funds, ETFs don't have investment minimums. Also, an ETF can offer more trading flexibility since it trades on an exchange (like a stock) throughout the day, with prices fluctuating continuously.

In the world of investing, balance is having the right mix of investments (or assets) in your portfolio to help reach your goals.

Over time, deposits, withdrawals and performance can cause your portfolio to drift from its original mix. To help keep your portfolio on track, we will buy or sell the appropriate exchange-traded funds (ETFs) to rebalance your portfolio.

An investment portfolio is a container that holds all your investments...like stocks, ETFs, mutual funds and cash.

At RBC InvestEase, our portfolios are made up of ETFs and cash.

An asset class is a grouping of investments that share similar features. Stocks (equities) and fixed income investments, such as bonds, are two of the main types of asset classes. Cash and cash equivalents is the third most common type of asset class.

The Management Expense Ratio (MER) includes a few different costs:

Investment funds pay investment fund managers a fee for managing their funds. You are not directly charged the management fee. But, these fees affect you because they reduce the amount of the fund’s return to you. Information about management fees and other charges to your investment funds is included in the prospectus or fund facts document for each fund.

See our FAQs for a detailed explainer.

Les régimes de placement enregistrés offrent des avantages fiscaux uniques qui vous aident à épargner pour l’avenir. Les caractéristiques, les avantages et les règles applicables aux régimes enregistrés sont établis par le gouvernement du Canada.

Les régimes de placement enregistrés offrent des avantages fiscaux uniques qui vous aident à épargner pour l’avenir. Les caractéristiques, les avantages et les règles applicables aux régimes enregistrés sont établis par le gouvernement du Canada.

Grâce au Régime d’accession à la propriété du gouvernement fédéral, vous pouvez puiser jusqu’à 60 000 $ dans votre Régime enregistré d’épargne-retraite (REER) (120 000 $ pour un couple) pour effectuer la mise de fonds sur votre première maison.

Pour utiliser les fonds de votre REER, ceux-ci doivent y avoir été déposés depuis au moins 90 jours. Vous devez avoir signé un contrat d’achat ou de construction d’un logement admissible.

Le grand avantage de cette option est que le retrait n’est pas imposable à condition que vous le remboursiez dans un délai de 15 ans. Le montant du remboursement annuel doit être d’au moins un quinzième du montant retiré de votre REER.

Les FNB sont conçus pour détenir des actions et des obligations dans un seul et même contenant. Ce contenant est un fonds que vous pouvez acheter.

Bien qu'ils soient similaires aux fonds communs de placement, les FNB n'ont pas de minimum d'investissement. De plus, un FNB offre une plus grande flexibilité de négociation puisqu'il est négocié en bourse (comme une action) tout au long de la journée, avec des cours qui fluctuent en permanence.

Vous savez que le fait de manger des fruits, des légumes, des protéines et des glucides sains favorise une alimentation équilibrée. Dans le monde des placements, on obtient cet équilibre en ayant une composition de l’actif qui aide à atteindre ses objectifs.

Au fil du temps, la composition de votre portefeuille peut changer en raison des dépôts, des retraits et des rendements. Pour vous aider à garder votre portefeuille sur la bonne voie, nous achèterons ou vendrons les FNB pertinents pour le rééquilibrer.

Une catégorie d’actifs est un regroupement de placements dont les caractéristiques sont semblables. Les actions (titres) et les placements à revenu fixe, comme les obligations, sont deux des principales catégories de titres. Les espèces et quasi-espèces sont la troisième catégorie de titres en importance.

Le portefeuille de placement est le contenant qui renferme tous vos placements… comme des actions, des FNB, des fonds communs de placement et des liquidités.

Les portefeuilles de RBC Investi-Clic sont composés de FNB et de liquidités.

Le ratio des frais de gestion (RFG) englobe plusieurs frais :

Les fonds de placement paient des frais aux gestionnaires de fonds. Ces frais de gestion ne vous sont pas facturés directement. Ils vous concernent toutefois, car ils viennent réduire le rendement de vos placements. Des renseignements sur les frais, dont les frais de gestion, sont fournis dans le prospectus ou le document Aperçu du fonds de chaque fonds.

Vous trouverez une explication plus détaillée dans notre FAQ.